Blog by Alex Lenferna, a divest-invest advocate and researcher getting his PhD in philosophy at the University of Washington, focusing on the ethics of climate change. His research and articles are freely available here.

It will come as no surprise to many that fossil fuel giant Exxon Mobil is underestimating the risks that climate change poses to its business model. Now, thanks in part to Exxon, we have a rather brilliant report from the Carbon Tracker Initiative which shows just how. The Carbon Tracker report comes in response to an analysis of the carbon bubble entitled Energy and Carbon – Managing the Risks, which Exxon released in response to pressure from shareholders. If the Carbon Tracker report is right, however, then Exxon is quite clearly not managing those risks and is instead inflating them.

According to the report, Exxon is “significantly underestimating the risks to its  business model from investments in higher cost, higher carbon reserves; increasing national and subnational climate regulation; competition from renewables; and demand stagnation.” What’s more, the risks to Exxon’s business are not a distant worry; rather they are already playing out. Exxon has seen a decline in return on their investments and is already underperforming. Carbon Tracker argues that this is partly as a result of Exxon taking on more and more high cost and low return projects such as oil sands, Arctic oil, and heavy oil. This represents an on-going trend whereby Exxon has been steadily replacing low cost high return production with high cost, low return and generally high carbon production.

business model from investments in higher cost, higher carbon reserves; increasing national and subnational climate regulation; competition from renewables; and demand stagnation.” What’s more, the risks to Exxon’s business are not a distant worry; rather they are already playing out. Exxon has seen a decline in return on their investments and is already underperforming. Carbon Tracker argues that this is partly as a result of Exxon taking on more and more high cost and low return projects such as oil sands, Arctic oil, and heavy oil. This represents an on-going trend whereby Exxon has been steadily replacing low cost high return production with high cost, low return and generally high carbon production.

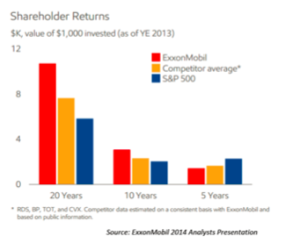

The result is poor performance from the oil industry’s once golden boy. For 40 years Exxon outperformed the market, but for the past five years it has dragged behind. Drawing on Exxon’s own analysis, Carbon Tracker’s report shows that if you invested in Exxon stock in 2009, your returns would be just 60 percent what you could’ve earned by investing in the S&P Index. This decrease in performance is arguably a potent omen of the unfurling carbon bubble and an incredible sign of the times. Indeed, Exxon Mobil, the world’s most profitable public fossil fuel company in history, is beginning to dramatically underperform relative to the broader stock market.

If Carbon Tracker is right, this is not a temporary blip, but rather this trend of underperformance is set to continue and deepen moving forward.

As Carbon Tracker points out, Exxon’s future plans are based on their own highly favourable assumptions and definitions, along with quite ‘creative’ (read: potentially intentionally deceitful) cherry-picking of data. Exxon’s projections painted a business-as-usual picture that showed them continuing profitably into the future, but the likelihood of that picture turning out to be true is increasingly slim given the rapidly changing energy market and regulatory landscape.

It’s been clear for a while that Exxon is betting on and supporting climate failure, and now we know the scale of that bet. Exxon for a number of problematic reasons does not really countenance the possibility of serious action on climate change and goes so far as to base its plans and projections on an International Energy Agency scenario that assumes no new climate policy. Betting on such a future seems an incredibly bad bet, especially with a flurry of new climate policy being put in place, and COP 21 just around the corner, which is set to see a suite of new more ambitious climate commitments come into place. Exxon’s report thus drastically underestimates the possibility of a low carbon future, a bet will likely turn out to be a bad one as the Carbon Tracker report adeptly highlights.

Not only is Exxon betting on climate failure, it is also betting on an incredibly high oil price, which seems unlikely to hold moving forward. Betting on such a high price is a risky bet indeed, for while costs of extraction are increasing, demand is flat and falling in developed nations, totally counter to oil company projections. According to a study by HSBC, lower oil prices are one of the main potential threats to shareholder returns for fossil fuel companies, for if oil prices are lower than projected then fossil fuel companies will not get adequate return on their investments. However, instead of internalizing the risk that oil prices may not be as high, Exxon is putting increasingly more capital investments into oil projects which rely on a high price to break even. As the Carbon Tracker report highlights, out of Exxon’s $286 billion in potential upstream oil capex from 2014—2025, $103 billion (36%) is for projects requiring a market price above $95/bbl.

As Ceres’ Andrew Logan and Ryan Salmon previously pointed out, Exxon is betting on a high demand for oil in order to keep a high price of oil, but if the price of oil does rise that high “consumers will use less oil as alternatives become more economic… [Thus] the oil industry could be facing a shrinking window of opportunity, making companies like Exxon Mobil vulnerable to any scenario other than” their own. Exxon’s outlook, furthermore, is looking increasingly unlikely.

Revealing Exxon’s worry about the fossil fuel divestment movement’s potential, it recently denounced the movement as being “out of step with reality”, but what the Carbon Tracker report makes clear is that it is Exxon who is arguably out of touch. Exxon claim that their investments in fossil fuels are a solution to global poverty, but such an argument is an insult to the global poor who are already and will increasingly be devastated by the ravages of climate change. Furthermore, Exxon’s prognosis is out of touch with the reality of affordable and sustainable energy for all, which would be much more effective at tackling global poverty, a point which the Carbon Tracker report adeptly expands on.

Given Exxon’s problematic plans, Carbon Tracker recommends that Exxon follow the example of Conoco oil and shrink in order to grow, by decreasing its investments in risky capital and carbon intensive projects. More specifically, the report recommends that Exxon “select only high return projects and yet still deliver growth to shareholders by redeploying capital that would otherwise have been invested in low return projects in to buybacks or special dividends ”. However, as the report further points out, “it is often difficult for incumbents [such as Exxon] to accept that change may be possible, indeed probable, until it is too late”. Thus the decline Exxon is experiencing will likely continue and get worse going into the future “unless management changes”, CTI warns.

Given the shrinking carbon budget, increasing action on climate change and a changing energy landscape, Exxon would perhaps do well to heed Carbon Tracker’s advice.

The Exxon report is the second of its kind from Carbon Tracker who had previously responded to Shell’s own such analysis of the carbon bubble. In that their response to Shell Carbon Tracker showed that $77 billion-worth of Shell’s new fossil fuel projects could be stranded as a result of climate change policies and a shifting energy landscape. What’s more Exxon and Shell’s plans and actions all form part of a broader trend whereby fossil fuel companies are acting in ways blind to these risks and are sinking more money into high capital low return investments. As a result more and more of the industry are seeing declines in their overall returns alongside significantly increased debt.

As Ambrose-Evans Pritchard reported in the Telegraph “the world’s leading oil and gas companies are taking on debt and selling assets on an unprecedented scale to cover a shortfall in cash, calling into question the long-term viability of large parts of the industry.” In fact, as the US Energy Information Agency recently highlighted, oil and gas companies took on $110 billion more in debt than they received in revenue returned during the last financial year. This trend is not likely to slow as fossil fuel companies are pouring more and more money into high cost low return projects. By investing in high capital low return oil projects, oil companies are putting approximately $1.1 trillion dollars at risk in just the coming decade, as was highlighted in an earlier Carbon Tracker report.

As Carbon Tracker’s latest analysis of the fossil fuel industry’s titans makes clear, the times are rapidly changing, and the continued profitability of investing in oil and gas companies is no longer a given.